Why SME travel buyers are rethinking policy, service, and technology

BTN’s 2026 SME research shows that small and midsize companies are not pulling back on travel. Instead, many are trying to bring more structure to programs that have become too large, too complex, or too visible to manage informally.

July 13, 2026

Small and midsize companies are still traveling. The bigger question is how well their travel programs can keep up.

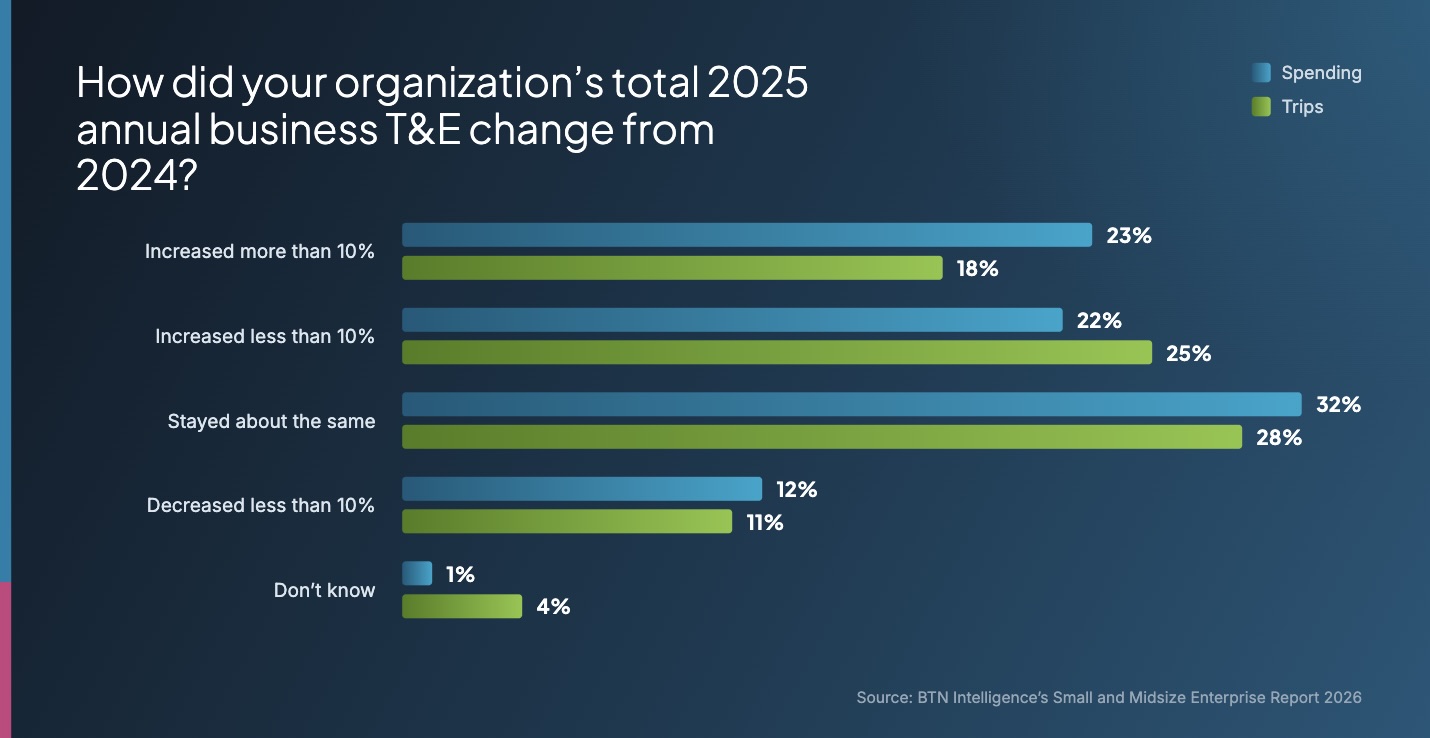

Business Travel News’ 2026 SME research points to a market where travel demand remains strong, even as cost pressure, geopolitical uncertainty, policy complexity, and traveler expectations all compete for attention. BTN reported that 45% of SME survey respondents said their organizations spent more on travel and entertainment in 2025 than they did the year before, while another 32% said spend stayed roughly the same.

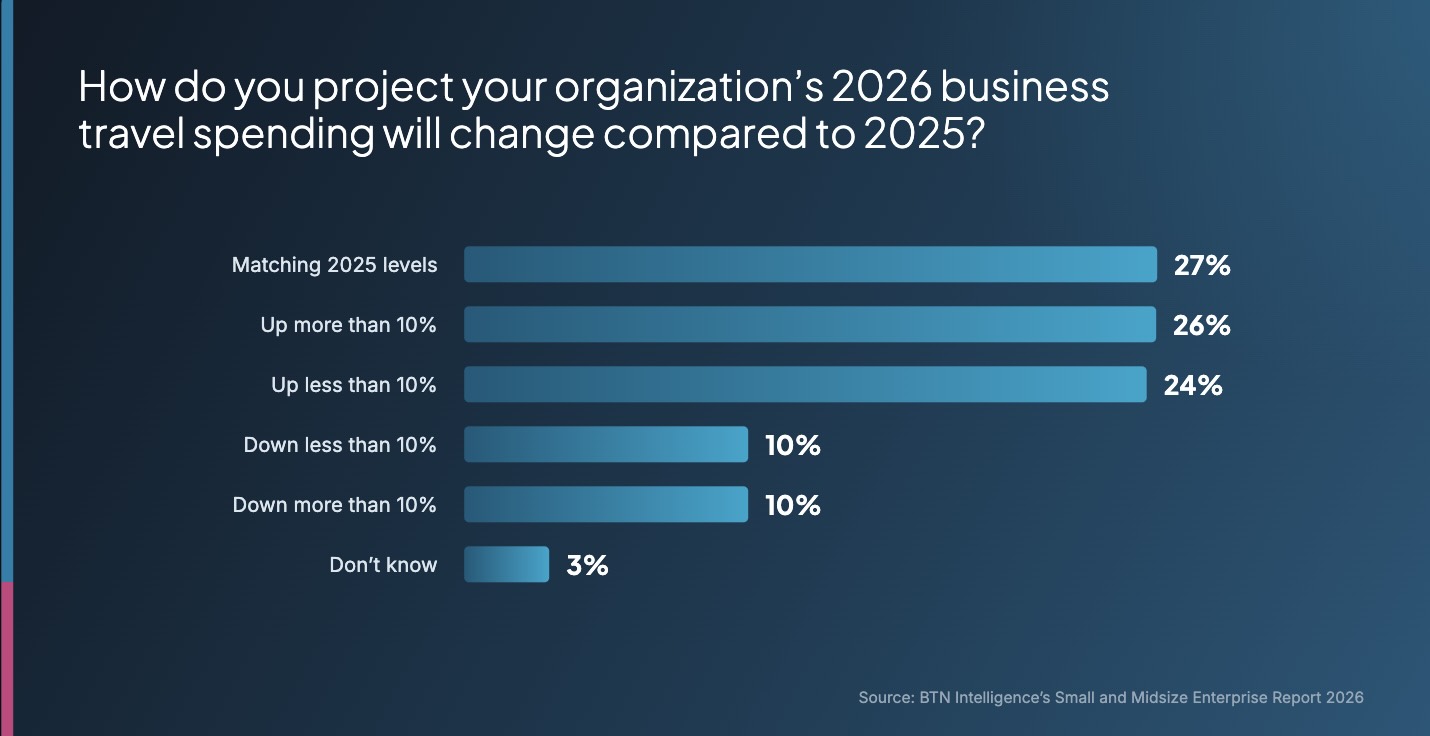

The same research suggests that many SMEs are not responding to higher costs by simply cutting travel. Instead, they are looking for more structure. BTN found that half of all respondents expected their organizations to increase 2026 travel spending year over year, while about 20% expected spending to decline.

That creates a familiar but difficult mandate for travel managers: support business growth, manage cost, protect travelers, improve visibility, and keep the traveler experience from becoming a reason people book outside the program.

For SMEs, the work is becoming less about deciding whether travel should happen and more about deciding how travel should be managed.

Travel demand is rising, but so is the need for control

BTN’s survey showed that higher travel spending is not limited to the largest programs. Among companies with at least $8 million in 2025 travel and entertainment spend, 56% reported a year-over-year spending increase. Among smaller organizations, 39% reported an increase.

Those numbers matter because travel growth tends to expose weak points in a program. A process that works for a handful of travelers can break down when more employees are booking trips, using different channels, submitting expenses late, or making policy decisions without clear guidance.

Jeffrey Madsen, VP of Product at Christopherson, described many SME programs as being “somewhere between basic and scaling.”

“They have vendor relationships and some kind of policy, but it’s often informal or undocumented,” Madsen said.

That middle stage is often where travel programs feel the most strain. The company has enough travel activity to need visibility and control, but not always enough internal staff to manage the program like a large enterprise would.

Madsen said the shift usually becomes more urgent as travel spend grows.

“The bigger maturity jump tends to happen between $500K and $2M in annual travel spend, which is when manual processes really start to break, and finance pushes for more structure,” he said.

BTN’s reporting supports that pattern. Cost control appeared repeatedly as both a priority and a challenge for SME travel managers, but the responses BTN cited pointed less toward blanket cuts and more toward stronger program management: better digital tools, more integrated travel and expense processes, stronger supplier partnerships, and policies designed to improve visibility and duty of care.

Policy is becoming a management tool, not just a document

The clearest shift in BTN’s 2026 SME research may be the role of travel policy.

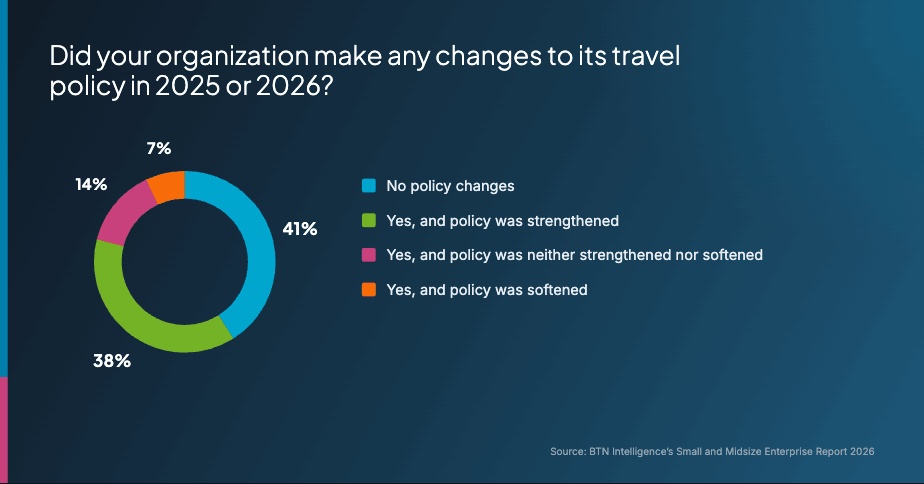

BTN reported that 59% of survey respondents said their organizations had altered their business travel policy either this year or last year. Of those that made changes, nearly two-thirds said the changes made the policy stronger, while a little more than one in 10 said their organization softened policy.

That does not necessarily mean SMEs are becoming rigid. The more interesting trend is that policy is becoming both more structured and more practical.

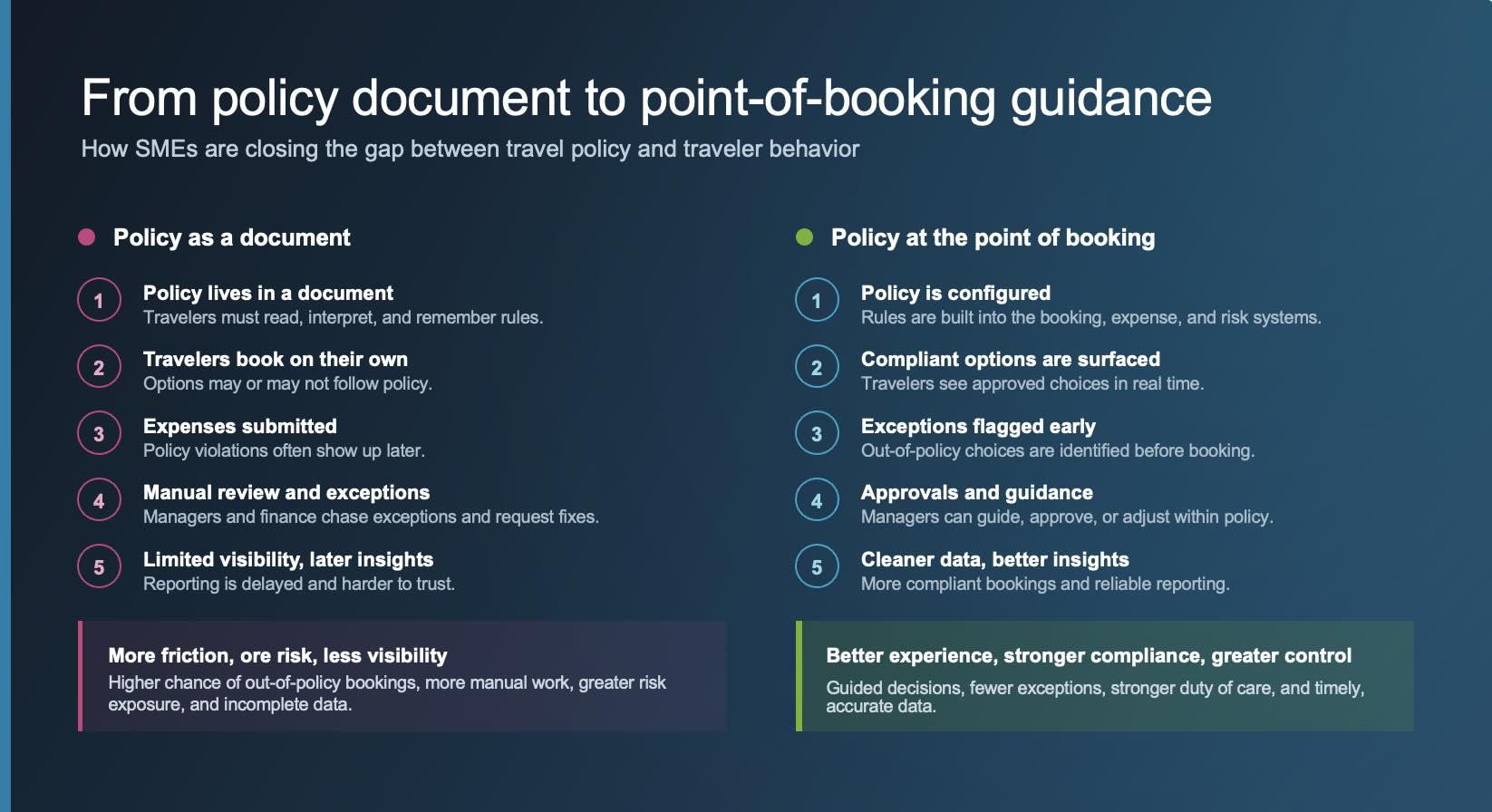

“The policy itself is getting tighter: clearer rules, configured into the booking flow, better data on compliance,” Madsen said. “But the experience around it is getting more flexible.”

That balance matters because strict policy language alone rarely changes traveler behavior. If the approved booking path is slower, more confusing, or more expensive than the options travelers can find on their own, companies risk losing the very visibility they are trying to create.

“The companies getting it right are tightening the rules while loosening the enforcement style,” Madsen said.

In practice, that means policy is moving closer to the point of decision. Instead of asking travelers to remember a PDF, companies are trying to surface compliant choices during search and booking, flag out-of-policy options earlier, and route exceptions before they become expense-report problems.

BTN described this as a broader shift in how technology shapes policy. According to BTN’s policy reporting, technology is increasingly becoming the mechanism companies use to shape traveler behavior and enforce policy more naturally.

Madsen put it more directly: “Policy used to live in a document. Now it’s configuration.”

Cost control is moving earlier in the trip

Cost control remains a central pressure point, but BTN’s research suggests SMEs are trying to manage cost before spend happens, not only after finance reviews it.

That is a meaningful change. Traditional travel controls often show up late in the process: after the traveler books, after the trip happens, after receipts are submitted, or after finance identifies the variance. By then, the organization may understand the problem, but it cannot always change the cost.

Madsen said more companies are setting cost expectations earlier.

“We’re also seeing a shift toward setting budgets upfront instead of reconciling spend after the fact,” he said. “Rather than approving a trip and finding out what it cost weeks later, companies are setting a per-trip budget and enforcing it at the point of booking.”

That approach also changes the conversation with travelers. Instead of a vague instruction to “book reasonably,” the traveler gets a clearer spending envelope. Finance gets better visibility. The travel manager gets fewer surprises after the trip.

BTN’s research also showed that external conditions are still shaping travel budgets. Survey respondents rated the impact of rising fuel costs and airfares on 2026 travel spending at 3.17 on a five-point scale, and recent geopolitical concerns at 3.33.

Those ratings do not suggest panic. They do suggest that SMEs are operating in a market where cost and risk can change quickly. A more structured program gives travel leaders a better way to respond without relying on broad restrictions that may cut into business activity.

“Travel itself isn’t being scaled back,” Madsen said. “What we’re seeing is companies getting more deliberate about which trips earn the investment, rather than cutting across the board.”

Duty of care is no longer only an enterprise concern

BTN’s 2026 SME research also shows how much risk management has moved into the SME conversation.

BTN reported that only 7% of respondents said their organizations do not actively manage travel risk. About 29% said they have formal, comprehensive travel risk management programs, while 37% said they have some processes in place but not a fully developed program. Another 27% said they manage travel risk informally or case by case.

That leaves many SMEs in a middle position. They understand the duty-of-care need, but their process may not be fully built.

The gap becomes more important as travel becomes more international. BTN found that 92% of respondents have responsibility for travel management in the United States, but only 32% have responsibility for the U.S. alone.

Madsen said duty of care has become a baseline expectation for many smaller and midsize programs.

“Duty of care isn’t really optional anymore, even at the small end of the SME market,” he said. “Any company with international travelers, healthcare workers in the field, or people in volatile regions now expects itinerary-based tracking, contextual risk alerts, and a defined emergency response.”

That expectation ties back to policy and booking behavior. If travelers book outside approved channels, the company may lose visibility into where they are, when plans change, or whether they need support during a disruption.

For travel managers, that makes traveler adoption more than a convenience issue. It becomes part of risk management.

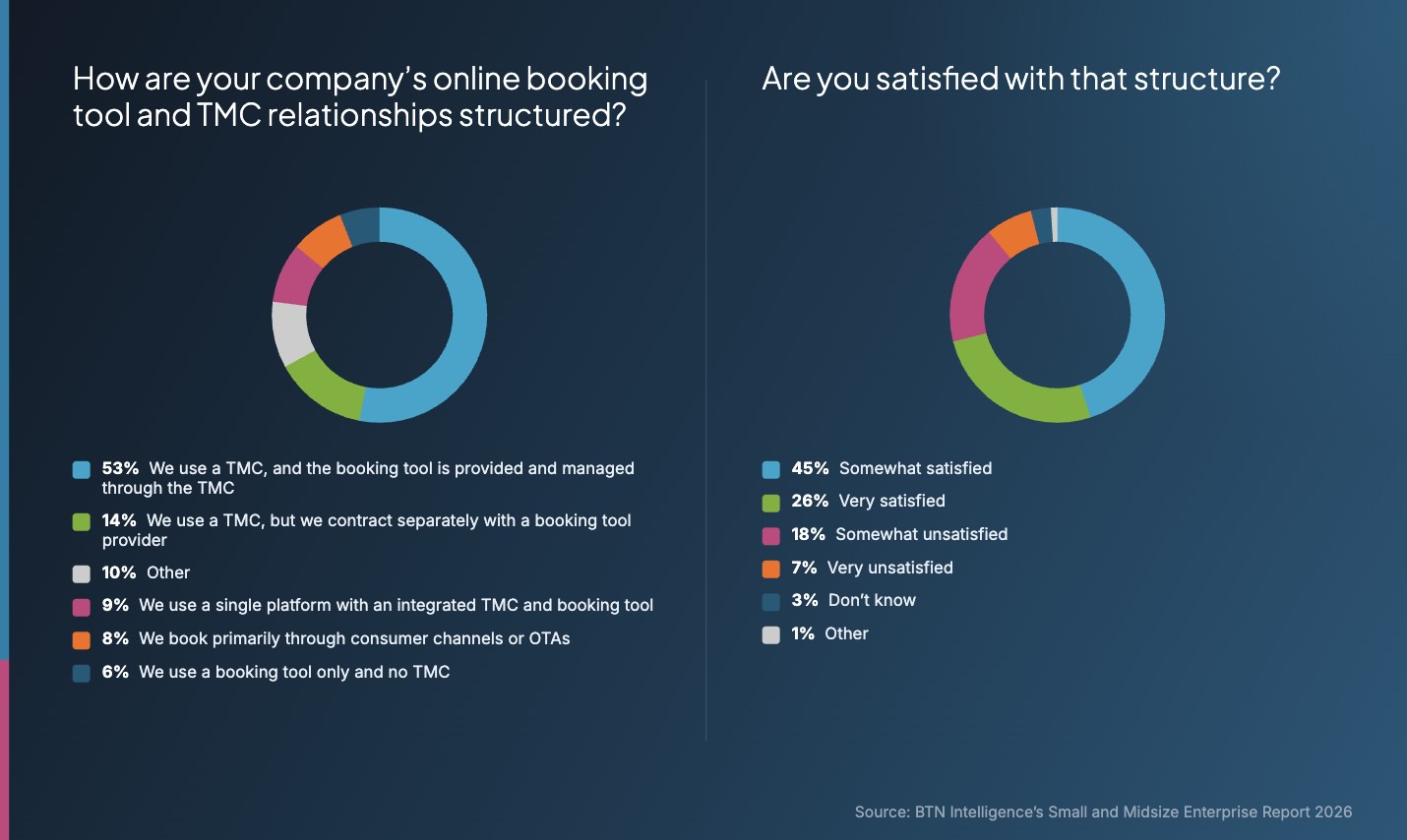

Only 26% of BTN survey respondents said they were “very satisfied” with their current TMC and booking tool arrangement, while 45% said they were “somewhat satisfied.” BTN also reported that 53% of SME respondents use a TMC-provided booking tool, while only 9% use an integrated all-in-one platform.

The data points to a market in transition. Traditional TMC models still dominate the SME segment, but traveler expectations are increasingly shaped by consumer booking experiences. Buyers want technology that works, reporting that does not require manual cleanup, and service that can still respond when something goes wrong.

BTN summarized the core questions for SME buyers this way: Can the TMC do what the company needs? Will it be a real partner? Will the technology work for travelers? What will it cost?

Those questions are not new. What has changed is the tolerance for weak answers.

SME travel managers often have limited staff, limited time, and a broad set of responsibilities. They may not have a full travel department to clean up fragmented reporting, chase missing receipts, audit every exception, or troubleshoot every traveler complaint. The right partner has to reduce work, not simply add another system to manage.

The next phase of SME travel management is structure without unnecessary friction

Taken together, BTN’s 2026 SME research shows a clear direction: SME travel programs are maturing.

Travel is not disappearing from the budget. Policy is becoming stronger. Technology is moving closer to the point of booking. Duty of care is becoming more formal. TMC relationships are being judged not only on price, but on whether the service model and technology can support the way the company actually operates.

The challenge is that more structure can create friction if it is not designed carefully. A stronger policy can improve compliance, but only if travelers can follow it. Better reporting can support smarter decisions, but only if the data is usable. More booking control can improve visibility, but only if the approved path works well enough that employees stay inside it.

For travel managers, the lesson is not to copy the largest enterprise programs. SMEs need structure that fits their size, travel patterns, staffing model, and growth stage.

That may mean formalizing a policy that has lived informally for years. It may mean building approvals or budget guidance earlier in the booking process. It may mean choosing a partner that can connect policy, service, reporting, payment, and traveler support without making the program harder to run.

The companies that get this right will not just have more rules. They will have a travel program that gives finance clearer visibility, gives travelers a better path to compliant choices, and gives the business more confidence that travel spend is supporting the right work.

Christopherson helps organizations strengthen corporate travel programs with policy guidance, service, technology, reporting, and traveler support built around the way each business operates. To discuss how your travel program can support growth with more visibility and control, connect with Christopherson.